How to Dig Out of Student Loan Debt

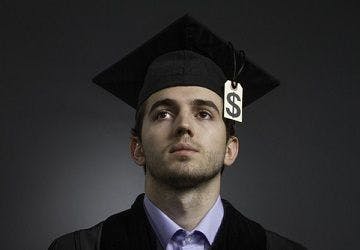

The average dental school graduate in 2016 left school with $261,149 in student loans, according to the American Dental Education Association (ADEA). More than 30 percent of grads reported debt of more than $300,000.

If you are like most dentists, you began your career under a massive debt load.

The average dental school graduate in 2016 left school with $261,149 in student loans, according to the American Dental Education Association (ADEA). More than 30 percent of grads reported debt of more than $300,000.

That doesn't include the cost of business loans to start a practice.

There are strategies you can use to cut down what you owe for your education. Attractive repayment programs, opportunities for loan forgiveness and smart money management can help you make your debt a thing of the past.

First, arm yourself with information about your own finances.

Create a personal budget that lists all of your expenses. You may think you know how you spend your money, but you'll probably find some surprises. Pay close attention to which of your expenses are fixed and necessary (such as a mortgage or car payment) and which are discretionary (such as dining out and entertainment costs).

Then make a list of all your current loan balances, interest rates and payback terms.

When you graduated with federal loans, unless you made other arrangements, you were probably put on a standard repayment plan with a 10-year payback schedule. Review all those terms and then get started.

Income-Driven Repayment Plans

Consider payment plans that are based on your income.

"Income-driven plans aren’t always the lowest payment but may still make sense in the early years of a career where the income is lower," said Diahann Lassus, a certified financial planner and certified public accountant with Lassus Wherley in New Providence, New Jersey. "There are many considerations including expected revenue growth of the practice, having a profit margin that can support not only the business debt but the student loan debt — and allow them to eat."

Here's a summary:

· Income-based repayment (IBR) offers payments equal to 10 percent of your discretionary income for new borrowers on or after July 1, 2014. The payments will never be more than your standard repayment plan amount. Those who borrowed before July 1, 2014, will have payments based on 15 percent of discretionary income, and again, never more than the standard repayment plan amount.

· Pay as you earn repayment (PAYE) has installments that are usually 10 percent of your discretionary income, but never more than the standard repayment plan amount.

· Revised pay as you earn repayment (REPAYE) will generally have payments that are 10 percent of your discretionary income.

· Under the income-contingent repayment (ICR) plan, you'll pay the lesser of 20 percent of your discretionary income or what you would pay on a repayment plan with a fixed payment over the course of 12 years, adjusted according to your income.

You can use the Department of Education's repayment estimator to see what your payments might be. The estimator can be found on the department’s website.

The income-driven plans will extend the number of years you have your loans, but you'll usually have lower interest rates than the standard 10-year plan. When your time is up (20 or 25 years depending on when you took your loans), the remainder of your debt may be forgiven.

That's really attractive, but there are caveats.

Your payments may change every year because you have to "recertify" your income and family size. As your income rises, your loan payments may, too.

"You may qualify one year, and be one dollar over the threshold and have to pay full payments the following year," said Chris Cooper, a San Diego, California-based certified financial planner.

Because the income-driven programs are over a longer time period, you'll pay significantly more in interest over the life of the loan.

Also be aware that if any of your loans are forgiven, you could be in for a big tax bill. The amount forgiven will be considered income, so you'll need to pay tax on that amount.

Loan Forgiveness

You can rid yourself of loans entirely with certain loan forgiveness programs, and so-called qualified forgiveness plans won't leave you with a tax burden.

If you work full-time for qualified employers such as government organizations or not-for-profits that are 501(c)(3) organizations, you may be able to join the Public Service

Loan Forgiveness

Program (PSLF), for direct loans. AmeriCorps and Peace Corps count, too.

To be considered a full-time worker, you must either work 30 hours a week or meet your employer's definition of full time, whichever is greater. If you have several part-time jobs at qualifying employers and you work a total of 30 hours per week, you may be eligible.

PSLF will forgive the remaining balance on your direct loans after you've made 120 payments under the plan.

If the remainder of your loans are forgiven, unlike the income-based repayment plans, you won't have a tax bill for the forgiven amount.

Other Government Programs

If you take the right job, you can get lots of help to pay off your debt.

National Health Service Corps (NHSC): Dentists can receive up to $50,000 for loan repayment for a promise of two years of service. You can serve longer for added loan repayment.

Indian Health Service Loan Repayment Program: For two years of service in the American Indian or Alaska Native communities, you can get up to $40,000. You can serve longer for added loan repayment.

Veterans Affairs: If you qualify, dentists who work for the Department of Veteran Affairs may earn up to $60,000 for loan repayment.

Army Dental Corps: You can receive up to $120,000 for loan repayment. The Army has other financial benefits such as signing bonuses.

Navy Health Professions Loan Repayment Program (HPLRP): You may qualify for up to $40,000 for loan repayment.

Air Force Dental Health Profession Scholarship Program (HPSP): In exchange for three years of service, you could qualify for free tuition and fees.

Ask your state: Many states offer loan repayment and forgiveness programs. Check your state to see its programs.

Refinancing

Refinancing student loans may help you get a lower interest rate and better terms. It will also simplify your finances by consolidating your loans into one monthly payment, which may lower your overall borrowing costs, Lassus said.

"When consolidating loans with the federal government as the lender, you have up to 30 years to repay your loans, the interest rate is a fixed weighted average of your previous loans and you have renewed eligibility for certain benefits," Lassus said. "Even if you have previously used deferments for unemployment or economic hardship, you will be eligible for them again."

But there are disadvantages.

By extending the loan term, you'll probably pay more in interest over the course of the loan.

And if you use a private lender, you'll lose important benefits of federal loans, including the chance to move to an income-based repayment plan, a forgiveness plan and hardship deferments.

Don't Use Your Home

It may be tempting to shift your student debt to your home by taking a home equity line of credit (HELOC) or home equity loan. Sure, you'll get an attractive interest rate and home loans are tax-deductible, but it's probably not worth the risk.

"Do not use a home equity loan, no matter how tempting it is — unless you have a guaranteed paycheck coming in and no one has that," Cooper said. "If you get behind on a home equity loan, the bank will foreclose on your house."